Why Prediction Markets Need

A Custom AMM

Traditional AMMs like Uniswap's CPMM weren't built for outcome tokens. Here's why that's a problem.

Inconsistent Liquidity

CPMM provides poor liquidity at extreme probabilities (near 0% or 100%), exactly when prediction markets need it most.

Unfair LP Losses

Loss-vs-rebalancing (LVR) spikes dramatically as expiration approaches and at edge prices, punishing liquidity providers unpredictably.

Time-Decay Volatility

Outcome token volatility depends on both price AND time remaining. Traditional AMMs ignore this critical factor.

Enter: Uniform AMM for Gaussian Score Dynamics

•pm-AMM uses mathematical optimization to ensure consistent LVR across all prices and times

The Innovation

- Models prediction markets as bets on Brownian motion (random walks)

- Derives optimal reserves using the normal distribution (Φ, φ functions)

- Achieves uniform LVR: losses proportional to pool value at any price

The Result

- 47% reduction in average LP losses vs CPMM

- Better liquidity at extreme probabilities (0.01 and 0.99)

- Predictable costs for liquidity providers

Why Morpheus?

Compare our approach with traditional AMMs and see the mathematical advantage

Uniform LVR across all prices

Optimal loss distribution

Consistent loss rate

Time-aware (dynamic variant)

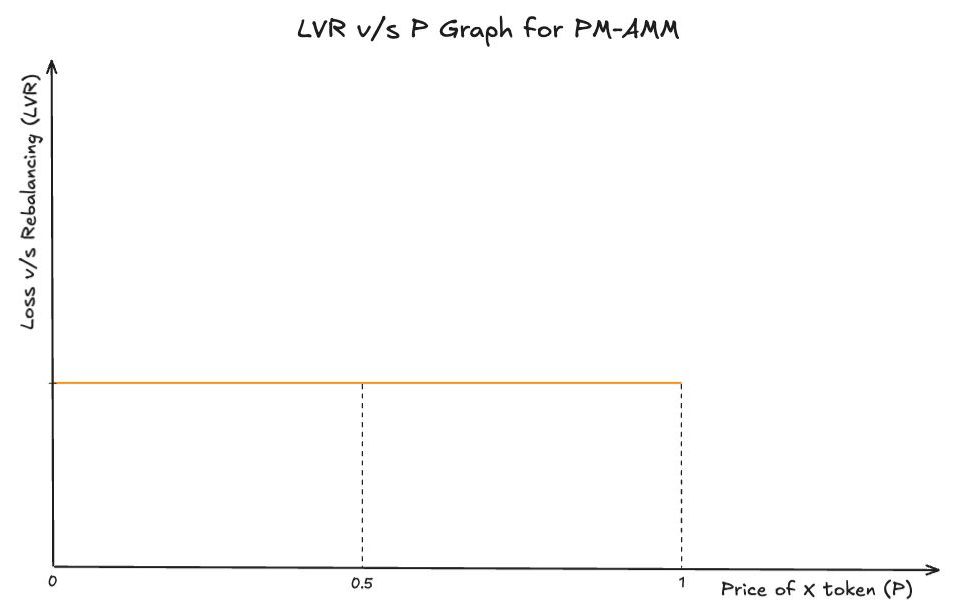

The pm-AMM achieves uniform Loss-vs-Rebalancing (LVR) across all prices, meaning the rate of loss to arbitrageurs is proportional to pool value regardless of current probability. This creates optimal risk distribution for prediction markets.

How It Works

The mathematical foundation behind optimal prediction market making

Model the Prediction Market

Gaussian Score Dynamics

We model the prediction market as a bet on whether an underlying Brownian motion (random walk) ends above zero at expiration time T.

The score process Z follows a random walk with volatility σ. Think: basketball score differential, vote margin, or price movements.

Brownian motion (random walk) representing the score differential

Built for Performance

Every feature designed with mathematical precision and real-world usability

Uniform LVR

Consistent losses for LPs regardless of price, making risk predictable and manageable

Better Liquidity

Concentrated around 50% probability where most trading happens, reducing slippage

Time-Aware

Dynamic variant adjusts liquidity over time to maintain constant expected LVR

Gas Optimized

Efficient approximations for normal distribution functions minimize computation costs

Full Analytics

Track LVR, pool value, trading volume, and compare performance vs alternatives

LP-First Design

Mathematical optimization ensures liquidity providers get fair, predictable returns

Ready to experience the future of prediction markets?

Join liquidity providers and traders already benefiting from mathematically optimal market making